𝗜𝗺𝗽𝗼𝗿𝘁𝗮𝗻𝘁 𝗖𝗼𝗻𝘁𝗲𝘅𝘁: 𝗪𝗲 𝗶𝗻𝗵𝗲𝗿𝗶𝘁𝗲𝗱 𝘁𝗵𝗶𝘀 𝗶𝗺𝗽𝗹𝗲𝗺𝗲𝗻𝘁𝗮𝘁𝗶𝗼𝗻 *years ago*. 𝗗𝘂𝗲 𝘁𝗼 𝘁𝗶𝗴𝗵𝘁 𝗽𝗿𝗼𝗷𝗲𝗰𝘁, 𝗰𝗼𝘀𝘁 𝗮𝗻𝗱 𝘁𝗶𝗺𝗲 𝗰𝗼𝗻𝘀𝘁𝗿𝗮𝗶𝗻𝘁𝘀, 𝘄𝗲 𝗰𝗼𝘂𝗹𝗱𝗻’𝘁 𝗽𝘂𝗿𝘀𝘂𝗲 𝗮𝗻𝘆 𝗼𝘁𝗵𝗲𝗿 𝗺𝗼𝗿𝗲 𝗼𝗽𝘁𝗶𝗺𝗮𝗹 𝘀𝗼𝗹𝘂𝘁𝗶𝗼𝗻𝘀 𝘀𝘂𝗰𝗵 𝗮𝘀 𝘁𝗵𝗲 𝗼𝗻𝗲𝘀 𝘀𝘂𝗴𝗴𝗲𝘀𝘁𝗲𝗱 𝗶𝗻 𝘁𝗵𝗲 𝗰𝗼𝗺𝗺𝗲𝗻𝘁𝘀.

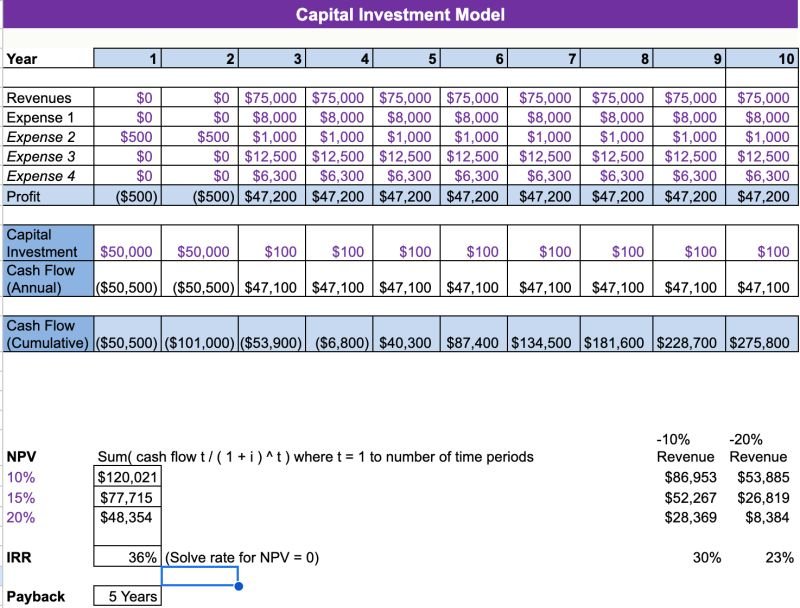

Imagine a capital investment model with columns for months and years, and many rows for revenues, expenses, profit, capital investment, annual cash flow, cumulative cash flow—plus a few rows for NPV and IRR. The image shows a vastly simplified model.

Now imagine implementing all of this in Salesforce for a big oil company. Not just the basic model, but also sensitivity analysis: what-if scenarios with, say, +10% expenses or -10% revenues — all this requiring recalculations of the entire model for every scenario. Needless to say, triggers weren't cutting it; recalculating everything was slow and even led to timeouts.

Almost a decade ago, we inherited this implementation and needed to fix it.

I suspected there was potential to leverage derivatives for sensitivity analysis to provide a faster and more efficient solution. But due to project and time constraints, we had to implement the entire recalculation approach instead - so there was some frustration because this was a sort of brute force approach.

Ultimately, we used asynchronous Apex to handle the heavy lifting, avoiding timeouts. But it was a pity that we couldn't optimize it further by determining the derivatives for NPV and IRR — a missed opportunity for a more elegant and faster solution.

For example, with the NPV formula, the derivative with respect to a cash flow would give an estimate of the change in NPV more directly, without recalculating everything. Using ΔNPV ≈ ΔC_t / (1 + i)^t would approximate the impact of changes in revenues or expenses, significantly speeding up sensitivity analysis (IRR would be more complicated though).

Have you ever faced a scenario where an optimal approach had to be put aside due to constraints? How did you handle it?